3. Default Risk and Income Fluctuations#

Contents

In addition to what’s in Anaconda, this lecture will need the following libraries:

!pip install --upgrade quantecon

Show code cell output

Requirement already satisfied: quantecon in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (0.7.2)

Requirement already satisfied: numba>=0.49.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from quantecon) (0.59.0)

Requirement already satisfied: numpy>=1.17.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from quantecon) (1.26.4)

Requirement already satisfied: requests in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from quantecon) (2.31.0)

Requirement already satisfied: scipy>=1.5.0 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from quantecon) (1.11.4)

Requirement already satisfied: sympy in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from quantecon) (1.12)

Requirement already satisfied: llvmlite<0.43,>=0.42.0dev0 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from numba>=0.49.0->quantecon) (0.42.0)

Requirement already satisfied: charset-normalizer<4,>=2 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from requests->quantecon) (2.0.4)

Requirement already satisfied: idna<4,>=2.5 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from requests->quantecon) (3.4)

Requirement already satisfied: urllib3<3,>=1.21.1 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from requests->quantecon) (2.0.7)

Requirement already satisfied: certifi>=2017.4.17 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from requests->quantecon) (2024.2.2)

Requirement already satisfied: mpmath>=0.19 in /home/runner/miniconda3/envs/quantecon/lib/python3.11/site-packages (from sympy->quantecon) (1.3.0)

3.1. Overview#

This lecture computes versions of Arellano’s [Arellano, 2008] model of sovereign default.

The model describes interactions among default risk, output, and an equilibrium interest rate that includes a premium for endogenous default risk.

The decision maker is a government of a small open economy that borrows from risk-neutral foreign creditors.

The foreign lenders must be compensated for default risk.

The government borrows and lends abroad in order to smooth the consumption of its citizens.

The government repays its debt only if it wants to, but declining to pay has adverse consequences.

The interest rate on government debt adjusts in response to the state-dependent default probability chosen by government.

The model yields outcomes that help interpret sovereign default experiences, including

countercyclical interest rates on sovereign debt

countercyclical trade balances

high volatility of consumption relative to output

Notably, long recessions caused by bad draws in the income process increase the government’s incentive to default.

This can lead to

spikes in interest rates

temporary losses of access to international credit markets

large drops in output, consumption, and welfare

large capital outflows during recessions

Such dynamics are consistent with experiences of many countries.

Let’s start with some imports:

import matplotlib.pyplot as plt

import numpy as np

import quantecon as qe

from numba import njit, prange

%matplotlib inline

3.2. Structure#

In this section we describe the main features of the model.

3.2.1. Output, Consumption and Debt#

A small open economy is endowed with an exogenous stochastically fluctuating potential output stream \(\{y_t\}\).

Potential output is realized only in periods in which the government honors its sovereign debt.

The output good can be traded or consumed.

The sequence \(\{y_t\}\) is described by a Markov process with stochastic density kernel \(p(y, y')\).

Households within the country are identical and rank stochastic consumption streams according to

Here

\(0 < \beta < 1\) is a time discount factor

\(u\) is an increasing and strictly concave utility function

Consumption sequences enjoyed by households are affected by the government’s decision to borrow or lend internationally.

The government is benevolent in the sense that its aim is to maximize (3.1).

The government is the only domestic actor with access to foreign credit.

Because household are averse to consumption fluctuations, the government will try to smooth consumption by borrowing from (and lending to) foreign creditors.

3.2.2. Asset Markets#

The only credit instrument available to the government is a one-period bond traded in international credit markets.

The bond market has the following features

The bond matures in one period and is not state contingent.

A purchase of a bond with face value \(B'\) is a claim to \(B'\) units of the consumption good next period.

To purchase \(B'\) next period costs \(q B'\) now, or, what is equivalent.

For selling \(-B'\) units of next period goods the seller earns \(- q B'\) of today’s goods.

If \(B' < 0\), then \(-q B'\) units of the good are received in the current period, for a promise to repay \(-B'\) units next period.

There is an equilibrium price function \(q(B', y)\) that makes \(q\) depend on both \(B'\) and \(y\).

Earnings on the government portfolio are distributed (or, if negative, taxed) lump sum to households.

When the government is not excluded from financial markets, the one-period national budget constraint is

Here and below, a prime denotes a next period value or a claim maturing next period.

To rule out Ponzi schemes, we also require that \(B \geq -Z\) in every period.

\(Z\) is chosen to be sufficiently large that the constraint never binds in equilibrium.

3.2.3. Financial Markets#

Foreign creditors

are risk neutral

know the domestic output stochastic process \(\{y_t\}\) and observe \(y_t, y_{t-1}, \ldots,\) at time \(t\)

can borrow or lend without limit in an international credit market at a constant international interest rate \(r\)

receive full payment if the government chooses to pay

receive zero if the government defaults on its one-period debt due

When a government is expected to default next period with probability \(\delta\), the expected value of a promise to pay one unit of consumption next period is \(1 - \delta\).

Therefore, the discounted expected value of a promise to pay \(B\) next period is

Next we turn to how the government in effect chooses the default probability \(\delta\).

3.2.4. Government’s Decisions#

At each point in time \(t\), the government chooses between

defaulting

meeting its current obligations and purchasing or selling an optimal quantity of one-period sovereign debt

Defaulting means declining to repay all of its current obligations.

If the government defaults in the current period, then consumption equals current output.

But a sovereign default has two consequences:

Output immediately falls from \(y\) to \(h(y)\), where \(0 \leq h(y) \leq y\).

It returns to \(y\) only after the country regains access to international credit markets.

The country loses access to foreign credit markets.

3.2.5. Reentering International Credit Market#

While in a state of default, the economy regains access to foreign credit in each subsequent period with probability \(\theta\).

3.3. Equilibrium#

Informally, an equilibrium is a sequence of interest rates on its sovereign debt, a stochastic sequence of government default decisions and an implied flow of household consumption such that

Consumption and assets satisfy the national budget constraint.

The government maximizes household utility taking into account

the resource constraint

the effect of its choices on the price of bonds

consequences of defaulting now for future net output and future borrowing and lending opportunities

The interest rate on the government’s debt includes a risk-premium sufficient to make foreign creditors expect on average to earn the constant risk-free international interest rate.

To express these ideas more precisely, consider first the choices of the government, which

enters a period with initial assets \(B\), or what is the same thing, initial debt to be repaid now of \(-B\)

observes current output \(y\), and

chooses either

to default, or

to pay \(-B\) and set next period’s debt due to \(-B'\)

In a recursive formulation,

state variables for the government comprise the pair \((B, y)\)

\(v(B, y)\) is the optimum value of the government’s problem when at the beginning of a period it faces the choice of whether to honor or default

\(v_c(B, y)\) is the value of choosing to pay obligations falling due

\(v_d(y)\) is the value of choosing to default

\(v_d(y)\) does not depend on \(B\) because, when access to credit is eventually regained, net foreign assets equal \(0\).

Expressed recursively, the value of defaulting is

The value of paying is

The three value functions are linked by

The government chooses to default when

and hence given \(B'\) the probability of default next period is

Given zero profits for foreign creditors in equilibrium, we can combine (3.3) and (3.4) to pin down the bond price function:

3.3.1. Definition of Equilibrium#

An equilibrium is

a pricing function \(q(B',y)\),

a triple of value functions \((v_c(B, y), v_d(y), v(B,y))\),

a decision rule telling the government when to default and when to pay as a function of the state \((B, y)\), and

an asset accumulation rule that, conditional on choosing not to default, maps \((B,y)\) into \(B'\)

such that

The three Bellman equations for \((v_c(B, y), v_d(y), v(B,y))\) are satisfied

Given the price function \(q(B',y)\), the default decision rule and the asset accumulation decision rule attain the optimal value function \(v(B,y)\), and

The price function \(q(B',y)\) satisfies equation (3.5)

3.4. Computation#

Let’s now compute an equilibrium of Arellano’s model.

The equilibrium objects are the value function \(v(B, y)\), the associated default decision rule, and the pricing function \(q(B', y)\).

We’ll use our code to replicate Arellano’s results.

After that we’ll perform some additional simulations.

We use a slightly modified version of the algorithm recommended by Arellano.

The appendix to [Arellano, 2008] recommends value function iteration until convergence, updating the price, and then repeating.

Instead, we update the bond price at every value function iteration step.

The second approach is faster and the two different procedures deliver very similar results.

Here is a more detailed description of our algorithm:

Guess a pair of non-default and default value functions \(v_c\) and \(v_d\).

Using these functions, calculate the value function \(v\), the corresponding default probabilities and the price function \(q\).

At each pair \((B, y)\),

update the value of defaulting \(v_d(y)\).

update the value of remaining \(v_c(B, y)\).

Check for convergence. If converged, stop – if not, go to step 2.

We use simple discretization on a grid of asset holdings and income levels.

The output process is discretized using a quadrature method due to Tauchen.

As we have in other places, we accelerate our code using Numba.

We define a class that will store parameters, grids and transition probabilities.

class Arellano_Economy:

" Stores data and creates primitives for the Arellano economy. "

def __init__(self,

B_grid_size= 251, # Grid size for bonds

B_grid_min=-0.45, # Smallest B value

B_grid_max=0.45, # Largest B value

y_grid_size=51, # Grid size for income

β=0.953, # Time discount parameter

γ=2.0, # Utility parameter

r=0.017, # Lending rate

ρ=0.945, # Persistence in the income process

η=0.025, # Standard deviation of the income process

θ=0.282, # Prob of re-entering financial markets

def_y_param=0.969): # Parameter governing income in default

# Save parameters

self.β, self.γ, self.r, = β, γ, r

self.ρ, self.η, self.θ = ρ, η, θ

self.y_grid_size = y_grid_size

self.B_grid_size = B_grid_size

self.B_grid = np.linspace(B_grid_min, B_grid_max, B_grid_size)

mc = qe.markov.tauchen(y_grid_size, ρ, η, 0, 3)

self.y_grid, self.P = np.exp(mc.state_values), mc.P

# The index at which B_grid is (close to) zero

self.B0_idx = np.searchsorted(self.B_grid, 1e-10)

# Output recieved while in default, with same shape as y_grid

self.def_y = np.minimum(def_y_param * np.mean(self.y_grid), self.y_grid)

def params(self):

return self.β, self.γ, self.r, self.ρ, self.η, self.θ

def arrays(self):

return self.P, self.y_grid, self.B_grid, self.def_y, self.B0_idx

Notice how the class returns the data it stores as simple numerical values and

arrays via the methods params and arrays.

We will use this data in the Numba-jitted functions defined below.

Jitted functions prefer simple arguments, since type inference is easier.

Here is the utility function.

@njit

def u(c, γ):

return c**(1-γ)/(1-γ)

Here is a function to compute the bond price at each state, given \(v_c\) and \(v_d\).

@njit

def compute_q(v_c, v_d, q, params, arrays):

"""

Compute the bond price function q(b, y) at each (b, y) pair.

This function writes to the array q that is passed in as an argument.

"""

# Unpack

β, γ, r, ρ, η, θ = params

P, y_grid, B_grid, def_y, B0_idx = arrays

for B_idx in range(len(B_grid)):

for y_idx in range(len(y_grid)):

# Compute default probability and corresponding bond price

delta = P[y_idx, v_c[B_idx, :] < v_d].sum()

q[B_idx, y_idx] = (1 - delta ) / (1 + r)

Next we introduce Bellman operators that updated \(v_d\) and \(v_c\).

@njit

def T_d(y_idx, v_c, v_d, params, arrays):

"""

The RHS of the Bellman equation when income is at index y_idx and

the country has chosen to default. Returns an update of v_d.

"""

# Unpack

β, γ, r, ρ, η, θ = params

P, y_grid, B_grid, def_y, B0_idx = arrays

current_utility = u(def_y[y_idx], γ)

v = np.maximum(v_c[B0_idx, :], v_d)

cont_value = np.sum((θ * v + (1 - θ) * v_d) * P[y_idx, :])

return current_utility + β * cont_value

@njit

def T_c(B_idx, y_idx, v_c, v_d, q, params, arrays):

"""

The RHS of the Bellman equation when the country is not in a

defaulted state on their debt. Returns a value that corresponds to

v_c[B_idx, y_idx], as well as the optimal level of bond sales B'.

"""

# Unpack

β, γ, r, ρ, η, θ = params

P, y_grid, B_grid, def_y, B0_idx = arrays

B = B_grid[B_idx]

y = y_grid[y_idx]

# Compute the RHS of Bellman equation

current_max = -1e10

# Step through choices of next period B'

for Bp_idx, Bp in enumerate(B_grid):

c = y + B - q[Bp_idx, y_idx] * Bp

if c > 0:

v = np.maximum(v_c[Bp_idx, :], v_d)

val = u(c, γ) + β * np.sum(v * P[y_idx, :])

if val > current_max:

current_max = val

Bp_star_idx = Bp_idx

return current_max, Bp_star_idx

Here is a fast function that calls these operators in the right sequence.

@njit(parallel=True)

def update_values_and_prices(v_c, v_d, # Current guess of value functions

B_star, q, # Arrays to be written to

params, arrays):

# Unpack

β, γ, r, ρ, η, θ = params

P, y_grid, B_grid, def_y, B0_idx = arrays

y_grid_size = len(y_grid)

B_grid_size = len(B_grid)

# Compute bond prices and write them to q

compute_q(v_c, v_d, q, params, arrays)

# Allocate memory

new_v_c = np.empty_like(v_c)

new_v_d = np.empty_like(v_d)

# Calculate and return new guesses for v_c and v_d

for y_idx in prange(y_grid_size):

new_v_d[y_idx] = T_d(y_idx, v_c, v_d, params, arrays)

for B_idx in range(B_grid_size):

new_v_c[B_idx, y_idx], Bp_idx = T_c(B_idx, y_idx,

v_c, v_d, q, params, arrays)

B_star[B_idx, y_idx] = Bp_idx

return new_v_c, new_v_d

We can now write a function that will use the Arellano_Economy class and the

functions defined above to compute the solution to our model.

We do not need to JIT compile this function since it only consists of outer loops (and JIT compiling makes almost zero difference).

In fact, one of the jobs of this function is to take an instance of

Arellano_Economy, which is hard for the JIT compiler to handle, and strip it

down to more basic objects, which are then passed out to jitted functions.

def solve(model, tol=1e-8, max_iter=10_000):

"""

Given an instance of Arellano_Economy, this function computes the optimal

policy and value functions.

"""

# Unpack

params = model.params()

arrays = model.arrays()

y_grid_size, B_grid_size = model.y_grid_size, model.B_grid_size

# Initial conditions for v_c and v_d

v_c = np.zeros((B_grid_size, y_grid_size))

v_d = np.zeros(y_grid_size)

# Allocate memory

q = np.empty_like(v_c)

B_star = np.empty_like(v_c, dtype=int)

current_iter = 0

dist = np.inf

while (current_iter < max_iter) and (dist > tol):

if current_iter % 100 == 0:

print(f"Entering iteration {current_iter}.")

new_v_c, new_v_d = update_values_and_prices(v_c, v_d, B_star, q, params, arrays)

# Check tolerance and update

dist = np.max(np.abs(new_v_c - v_c)) + np.max(np.abs(new_v_d - v_d))

v_c = new_v_c

v_d = new_v_d

current_iter += 1

print(f"Terminating at iteration {current_iter}.")

return v_c, v_d, q, B_star

Finally, we write a function that will allow us to simulate the economy once we have the policy functions

def simulate(model, T, v_c, v_d, q, B_star, y_idx=None, B_idx=None):

"""

Simulates the Arellano 2008 model of sovereign debt

Here `model` is an instance of `Arellano_Economy` and `T` is the length of

the simulation. Endogenous objects `v_c`, `v_d`, `q` and `B_star` are

assumed to come from a solution to `model`.

"""

# Unpack elements of the model

B0_idx = model.B0_idx

y_grid = model.y_grid

B_grid, y_grid, P = model.B_grid, model.y_grid, model.P

# Set initial conditions to middle of grids

if y_idx == None:

y_idx = np.searchsorted(y_grid, y_grid.mean())

if B_idx == None:

B_idx = B0_idx

in_default = False

# Create Markov chain and simulate income process

mc = qe.MarkovChain(P, y_grid)

y_sim_indices = mc.simulate_indices(T+1, init=y_idx)

# Allocate memory for outputs

y_sim = np.empty(T)

y_a_sim = np.empty(T)

B_sim = np.empty(T)

q_sim = np.empty(T)

d_sim = np.empty(T, dtype=int)

# Perform simulation

t = 0

while t < T:

# Store the value of y_t and B_t

y_sim[t] = y_grid[y_idx]

B_sim[t] = B_grid[B_idx]

# if in default:

if v_c[B_idx, y_idx] < v_d[y_idx] or in_default:

y_a_sim[t] = model.def_y[y_idx]

d_sim[t] = 1

Bp_idx = B0_idx

# Re-enter financial markets next period with prob θ

in_default = False if np.random.rand() < model.θ else True

else:

y_a_sim[t] = y_sim[t]

d_sim[t] = 0

Bp_idx = B_star[B_idx, y_idx]

q_sim[t] = q[Bp_idx, y_idx]

# Update time and indices

t += 1

y_idx = y_sim_indices[t]

B_idx = Bp_idx

return y_sim, y_a_sim, B_sim, q_sim, d_sim

3.5. Results#

Let’s start by trying to replicate the results obtained in [Arellano, 2008].

In what follows, all results are computed using Arellano’s parameter values.

The values can be seen in the __init__ method of the Arellano_Economy

shown above.

For example, r=0.017 matches the average quarterly rate on a 5 year US treasury over the period 1983–2001.

Details on how to compute the figures are reported as solutions to the exercises.

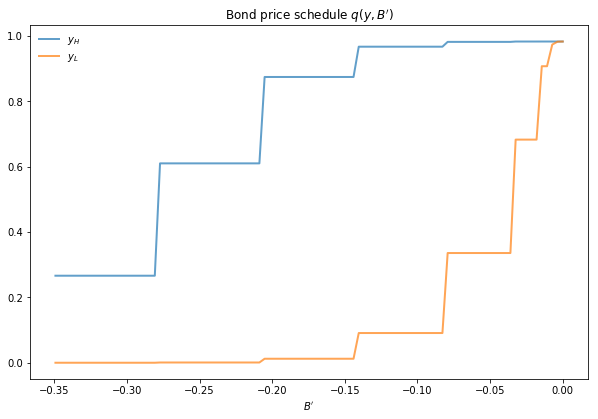

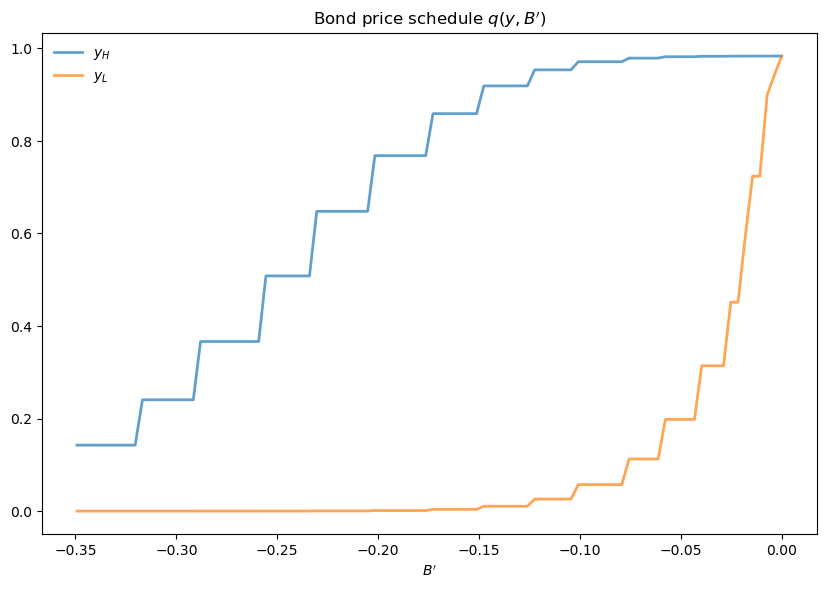

The first figure shows the bond price schedule and replicates Figure 3 of Arellano, where \(y_L\) and \(Y_H\) are particular below average and above average values of output \(y\).

\(y_L\) is 5% below the mean of the \(y\) grid values

\(y_H\) is 5% above the mean of the \(y\) grid values

The grid used to compute this figure was relatively fine (y_grid_size, B_grid_size = 51, 251), which explains the minor differences between this and

Arrelano’s figure.

The figure shows that

Higher levels of debt (larger \(-B'\)) induce larger discounts on the face value, which correspond to higher interest rates.

Lower income also causes more discounting, as foreign creditors anticipate greater likelihood of default.

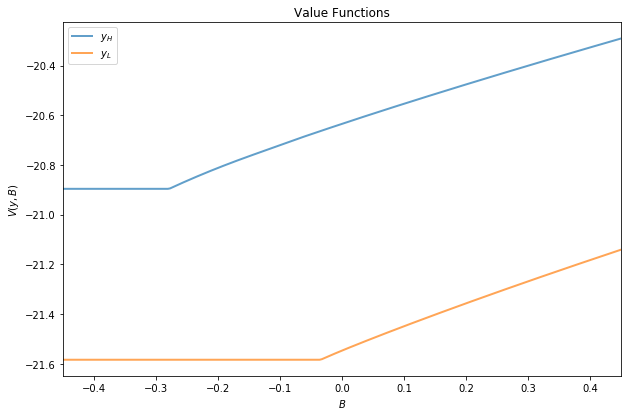

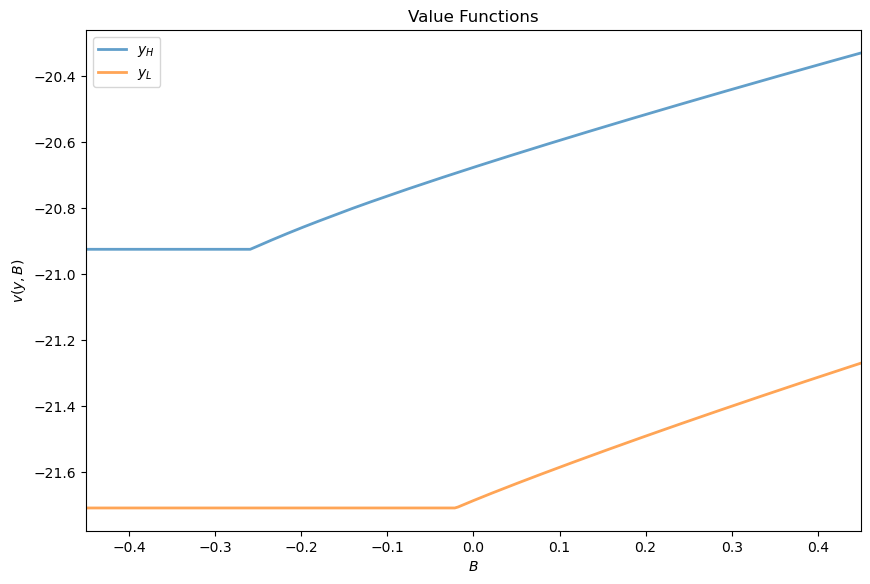

The next figure plots value functions and replicates the right hand panel of Figure 4 of [Arellano, 2008].

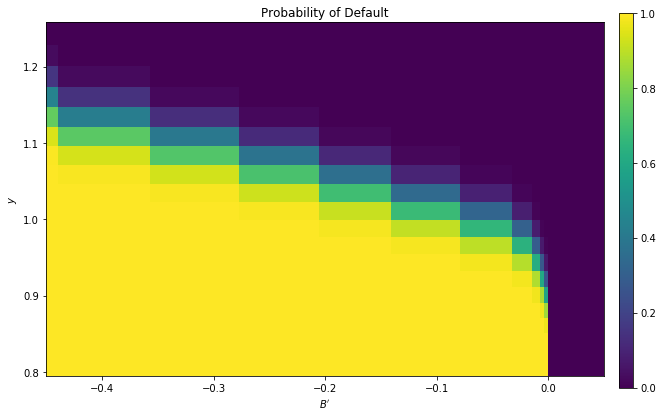

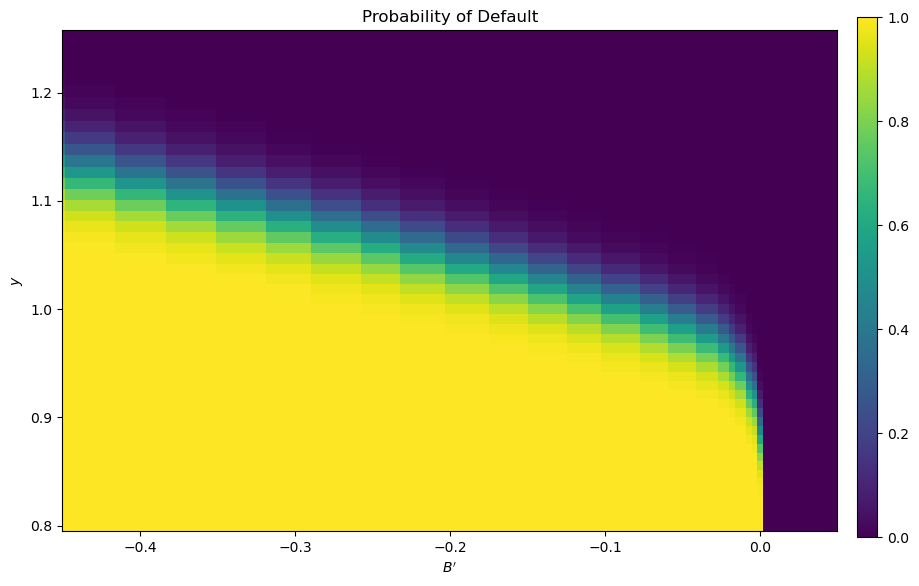

We can use the results of the computation to study the default probability \(\delta(B', y)\) defined in (3.4).

The next plot shows these default probabilities over \((B', y)\) as a heat map.

As anticipated, the probability that the government chooses to default in the following period increases with indebtedness and falls with income.

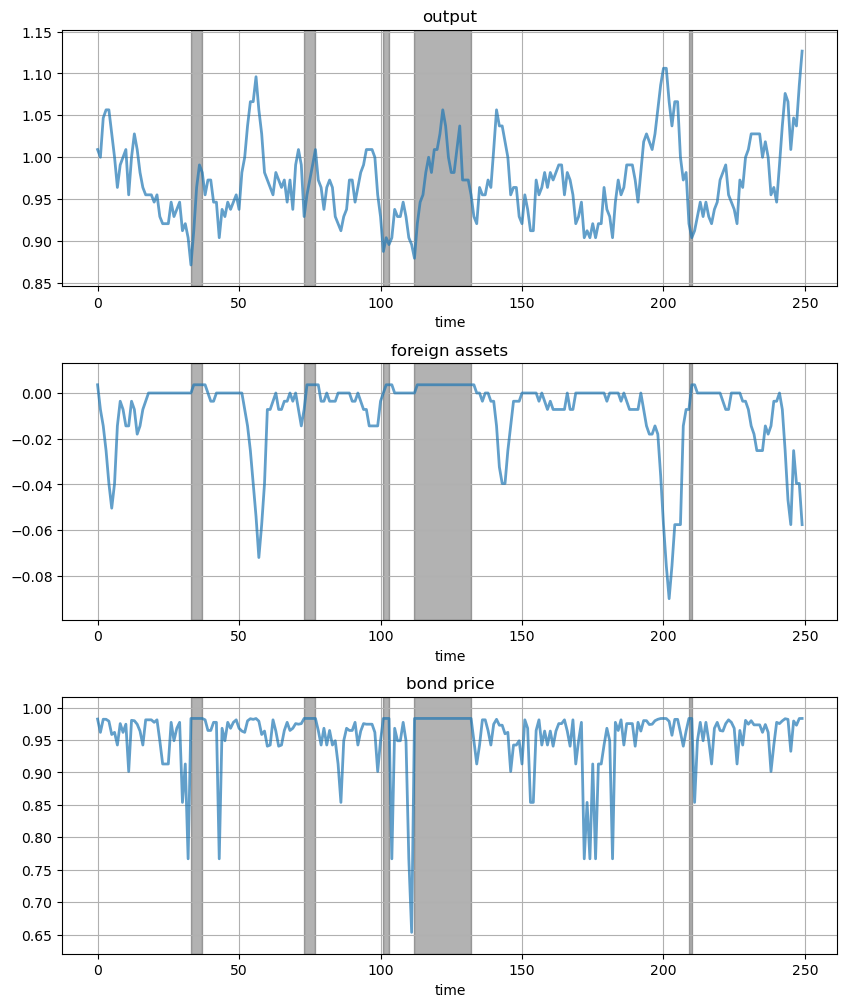

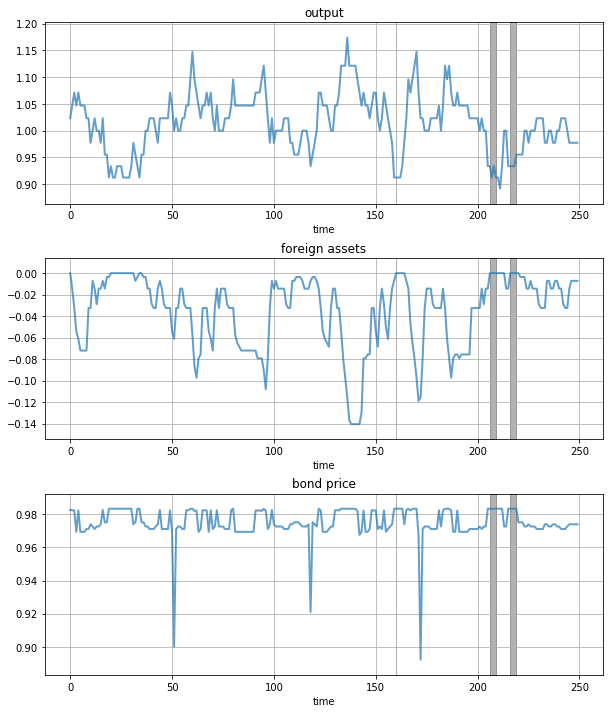

Next let’s run a time series simulation of \(\{y_t\}\), \(\{B_t\}\) and \(q(B_{t+1}, y_t)\).

The grey vertical bars correspond to periods when the economy is excluded from financial markets because of a past default.

One notable feature of the simulated data is the nonlinear response of interest rates.

Periods of relative stability are followed by sharp spikes in the discount rate on government debt.

3.6. Exercises#

Exercise 3.1

To the extent that you can, replicate the figures shown above

Use the parameter values listed as defaults in

Arellano_Economy.The time series will of course vary depending on the shock draws.

Solution to Exercise 3.1

Compute the value function, policy and equilibrium prices

ae = Arellano_Economy()

v_c, v_d, q, B_star = solve(ae)

Entering iteration 0.

Entering iteration 100.

Entering iteration 200.

Entering iteration 300.

Terminating at iteration 399.

Compute the bond price schedule as seen in figure 3 of Arellano (2008)

# Unpack some useful names

B_grid, y_grid, P = ae.B_grid, ae.y_grid, ae.P

B_grid_size, y_grid_size = len(B_grid), len(y_grid)

r = ae.r

# Create "Y High" and "Y Low" values as 5% devs from mean

high, low = np.mean(y_grid) * 1.05, np.mean(y_grid) * .95

iy_high, iy_low = (np.searchsorted(y_grid, x) for x in (high, low))

fig, ax = plt.subplots(figsize=(10, 6.5))

ax.set_title("Bond price schedule $q(y, B')$")

# Extract a suitable plot grid

x = []

q_low = []

q_high = []

for i, B in enumerate(B_grid):

if -0.35 <= B <= 0: # To match fig 3 of Arellano

x.append(B)

q_low.append(q[i, iy_low])

q_high.append(q[i, iy_high])

ax.plot(x, q_high, label="$y_H$", lw=2, alpha=0.7)

ax.plot(x, q_low, label="$y_L$", lw=2, alpha=0.7)

ax.set_xlabel("$B'$")

ax.legend(loc='upper left', frameon=False)

plt.show()

Draw a plot of the value functions

v = np.maximum(v_c, np.reshape(v_d, (1, y_grid_size)))

fig, ax = plt.subplots(figsize=(10, 6.5))

ax.set_title("Value Functions")

ax.plot(B_grid, v[:, iy_high], label="$y_H$", lw=2, alpha=0.7)

ax.plot(B_grid, v[:, iy_low], label="$y_L$", lw=2, alpha=0.7)

ax.legend(loc='upper left')

ax.set(xlabel="$B$", ylabel="$v(y, B)$")

ax.set_xlim(min(B_grid), max(B_grid))

plt.show()

Draw a heat map for default probability

xx, yy = B_grid, y_grid

zz = np.empty_like(v_c)

for B_idx in range(B_grid_size):

for y_idx in range(y_grid_size):

zz[B_idx, y_idx] = P[y_idx, v_c[B_idx, :] < v_d].sum()

# Create figure

fig, ax = plt.subplots(figsize=(10, 6.5))

hm = ax.pcolormesh(xx, yy, zz.T)

cax = fig.add_axes([.92, .1, .02, .8])

fig.colorbar(hm, cax=cax)

ax.axis([xx.min(), 0.05, yy.min(), yy.max()])

ax.set(xlabel="$B'$", ylabel="$y$", title="Probability of Default")

plt.show()

Plot a time series of major variables simulated from the model

T = 250

np.random.seed(42)

y_sim, y_a_sim, B_sim, q_sim, d_sim = simulate(ae, T, v_c, v_d, q, B_star)

# Pick up default start and end dates

start_end_pairs = []

i = 0

while i < len(d_sim):

if d_sim[i] == 0:

i += 1

else:

# If we get to here we're in default

start_default = i

while i < len(d_sim) and d_sim[i] == 1:

i += 1

end_default = i - 1

start_end_pairs.append((start_default, end_default))

plot_series = (y_sim, B_sim, q_sim)

titles = 'output', 'foreign assets', 'bond price'

fig, axes = plt.subplots(len(plot_series), 1, figsize=(10, 12))

fig.subplots_adjust(hspace=0.3)

for ax, series, title in zip(axes, plot_series, titles):

# Determine suitable y limits

s_max, s_min = max(series), min(series)

s_range = s_max - s_min

y_max = s_max + s_range * 0.1

y_min = s_min - s_range * 0.1

ax.set_ylim(y_min, y_max)

for pair in start_end_pairs:

ax.fill_between(pair, (y_min, y_min), (y_max, y_max),

color='k', alpha=0.3)

ax.grid()

ax.plot(range(T), series, lw=2, alpha=0.7)

ax.set(title=title, xlabel="time")

plt.show()